Share insight

Idea In Brief

Front line

Industry is on the front line of decarbonisation. From mine sites, smelters and refineries to corporate headquarters, businesses of all kinds are working out how to make their operations more sustainable.

Several considerations

Each industry has several high-level factors to consider in planning its transition, including their relationship to energy, technical and economic feasibility, and strategic use of assets.

Many questions

There are big questions for transition leaders, including what support should government provide, to what extent can a sector decarbonise, and what is the electricity profile of customers.

The Pathways to Net Zero series offers context, insights and key questions on different aspects of Australia’s transition to net zero. It builds on the groundbreaking research of Net Zero Australia. You can read earlier editions in the series on our website.

Industry is on the front line of Australia’s decarbonisation challenge. From mine sites, smelters and refineries to corporate headquarters, shopping centres and restaurants, businesses of all kinds are working out how to make their operations more sustainable.

While commercial considerations must be finely balanced in any strategy, much of the pressure for change is coming from capital markets. Some financiers now refuse to fund new coal exploration projects or seek a premium for their investment. Demands on companies are only likely to grow from socially conscious stakeholders, particularly as community expectations change and more millennials control the levers of wealth.

Government policy is also driving decarbonisation, following Australia’s commitment to achieve net-zero emissions by 2050 in line with the Paris Agreement. The Australian Government has introduced the Safeguard Mechanism that sets legislated limits on emissions at large industrial facilities. Internationally, the European Union’s Carbon Border Adjustment Mechanism will take effect in 2027. This is a tax on imported products, based on emissions generated during production, and likely the first of many such schemes among Australia’s trading partners.

The Net Zero Australia mobilisation report discusses potential technology options for heavy industry and the commercial sector. Each business needs to establish the best, most efficient approach based on its unique circumstances. This could involve electrifying industrial processes and vehicle fleets. It might mean switching to cleaner fuels and away from gas and diesel, modernising building footprints, pursuing abatement strategies such as revegetation, or even changing focus altogether (such as shifting from exporting iron ore to making steel).

Together, these decisions by industry represent the majority of the heavy lifting required to decarbonise the Australian economy.

What comes next?

Nous was pleased to contribute to the Net Zero Australia mobilisation report, which provides rigorous, independent analysis of how Australia can achieve net-zero emissions for its domestic and export economies. We believe each industry has several high-level factors to consider in planning its transition.

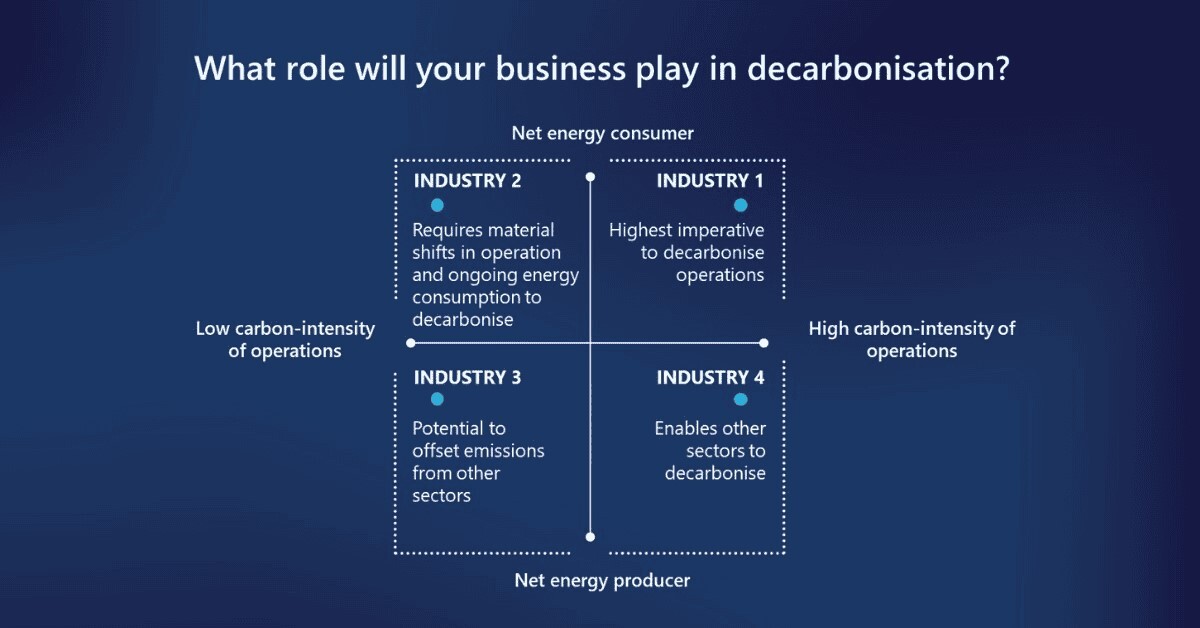

Some businesses produce energy while others consume it. Decarbonisation solutions will look different for ‘makers’ versus ‘takers’.

Energy producers are at the forefront of decarbonisation as coal plants shut down and new alternatives emerge, including renewable energy sources and battery storage. These businesses are positioned to assist others to reduce their emissions.

Another category of businesses primarily consume energy, but differ in their carbon intensity. For example, a shopping centre open during normal business hours will have different energy supply requirements to an around-the-clock mine site – which creates further emissions in the process of making another product such as cement or steel. It is also possible to distinguish between businesses that operate a stationary premises versus ones that involve a freight component, generating emissions across their entire vehicle fleet.

A common decarbonisation approach might involve seeking to save energy during periods of peak demand. A shopping centre could choose to increase the temperature setting on its air conditioners. By contrast, a steel producer could negotiate a more flexible contract in which electricity supply is reduced at times of day involving minimal business impact, in return for paying a lower rate.

Technical feasibility of low-emissions technologies must be balanced against economic feasibility.

Trade-offs are inevitable, as any switch to a new energy solution will be capital-intensive and businesses need supply chain certainty.

Some industries may consider pursuing renewable electricity, increasing their use of electric vehicles or improving their building’s energy efficiency. Businesses that embrace electrification must also consider the extent to which they rely on renewable supply from the grid or source their own, such as via solar generation.

Some industries may find that the most promising low-emissions technologies are still in their infancy or not yet proven at scale. Examples here include hydrogen-powered transport, carbon capture of process emissions, and permanent CO2 storage.

Invariably, organisations’ appetite for change will depend on their financial situation, and to what extent decarbonisation is a core priority. Decarbonisation strategies will depend on location factors such as grid access, renewable generation potential, access to renewable fuels, and CO2 transport and storage infrastructure.

Assets need to be considered strategically and gradually replaced where viable.

Across industries, one way to decarbonise is to replace existing assets with those that have lower carbon intensity. The pace at which this is done will depend on asset lifecycles and technological advancement.

As businesses look to reduce emissions from their built environments, we are seeing innovations such as skyscrapers being constructed using wood and other less carbon-intensive materials, along with smart technologies regulating energy and water use.

More generally, businesses need to consider the remaining lifespan of their assets (such as industrial equipment or vehicle fleets) and the trade-offs involved in replacing them.

The big questions for transition leaders

For government:

- As new technologies take time to become technologically viable, what support should government provide to assist businesses with the net-zero transition?

- What policies should be enacted to look after affected workers, particularly in fossil fuel-producing regions? Is it possible to locate new zero-carbon industries in areas impacted by business closures and job losses?

- How should the Australian Government balance and coordinate investment across states and territories?

- What trade, geopolitical and national security considerations are relevant to Australia’s role in global decarbonisation and how should these be addressed?

For business and industry:

- Realistically, to what extent can a particular business or industry sector decarbonise?

- Is there a trade-off between the technical and commercial viability of low-emissions technologies? Can the risks be managed, and do the benefits outweigh the costs?

- What do investors, shareholders and other stakeholders expect from the business?

- How should businesses begin to measure Scope 3 emissions (those generated by customers and supply chains)?

For power generators and retailers and other utilities:

- What is the electricity demand and supply profile of customers, now and into the future?

- How can portfolios be managed and balanced to provide a reliable energy supply offering a combination of long-, medium- and short-term duration storage and innovative supply contracts?

- Where gentailers are publicly owned, to what extent will the government as shareholder fund required infrastructure upgrades?

For financiers:

- How can capital allocation strategies be developed to prioritise Australia’s net-zero transition and incentivise businesses to change their behaviour?

Get in touch to discuss how these issues impact your organisation.

Connect with Wadzi Katsidzira and Craig Knox Lyttle on LinkedIn.

Prepared with input from Lynette Kotze during her time as a Director at Nous.

Authors

Wadzi Katsidzira

Director

Wadzi is a sustainability and social investment specialist leading projects in strategy, climate transition, portfolio management and program design.